In this lab we implement many of the techniques discussed in this chapter. We import some of our libraries at this top level.

from functools import partial

import numpy as np

import pandas as pd

import sklearn.linear_model as skl

import sklearn.model_selection as skm

from ISLP import load_data

from ISLP.models import ModelSpec as MS

from matplotlib.pyplot import subplots

from sklearn.preprocessing import StandardScaler

from statsmodels.api import OLSWe again collect the new imports

needed for this lab. Readers will also have to have installed l0bnb using pip install l0bnb.

from ISLP.models import Stepwise, sklearn_selected, sklearn_selection_path

from l0bnb import fit_path

from sklearn.cross_decomposition import PLSRegression

from sklearn.decomposition import PCA

from sklearn.pipeline import PipelineSubset Selection Methods¶

Here we implement methods that reduce the number of parameters in a model by restricting the model to a subset of the input variables.

Forward Selection¶

We will apply the forward-selection approach to the Hitters

data. We wish to predict a baseball player’s Salary on the

basis of various statistics associated with performance in the

previous year.

First of all, we note that the Salary variable is missing for

some of the players. The np.isnan() function can be used to

identify the missing observations. It returns an array

of the same shape as the input vector, with a True for any elements that

are missing, and a False for non-missing elements. The

sum() method can then be used to count all of the

missing elements.

Hitters = load_data("Hitters")

np.isnan(Hitters["Salary"]).sum()59We see that Salary is missing for 59 players. The

dropna() method of data frames removes all of the rows that have missing

values in any variable (by default --- see Hitters.dropna?).

Hitters = Hitters.dropna()

Hitters.shape(263, 20)We first choose the best model using forward selection based on (\ref{Ch6:eq:cp}). This score

is not built in as a metric to sklearn. We therefore define a function to compute it ourselves, and use

it as a scorer. By default, sklearn tries to maximize a score, hence

our scoring function computes the negative statistic.

def nCp(sigma2, estimator, X, Y):

"""Negative Cp statistic"""

n, p = X.shape

Yhat = estimator.predict(X)

RSS = np.sum((Y - Yhat) ** 2)

return -(RSS + 2 * p * sigma2) / nWe need to estimate the residual variance , which is the first argument in our scoring function above. We will fit the biggest model, using all the variables, and estimate based on its MSE.

design = MS(Hitters.columns.drop("Salary")).fit(Hitters)

Y = np.array(Hitters["Salary"])

X = design.transform(Hitters)

sigma2 = OLS(Y, X).fit().scaleThe function sklearn_selected() expects a scorer with just three arguments --- the last three in the definition of nCp() above. We use the function partial() first seen in Section~\ref{Ch5-resample-lab:the-bootstrap} to freeze the first argument with our estimate of .

neg_Cp = partial(nCp, sigma2)We can now use neg_Cp() as a scorer for model selection.

Along with a score we need to specify the search strategy. This is done through the object

Stepwise() in the ISLP.models package. The method Stepwise.first_peak()

runs forward stepwise until any further additions to the model do not result

in an improvement in the evaluation score. Similarly, the method Stepwise.fixed_steps()

runs a fixed number of steps of stepwise search.

strategy = Stepwise.first_peak(design, direction="forward", max_terms=len(design.terms))We now fit a linear regression model with Salary as outcome using forward

selection. To do so, we use the function sklearn_selected() from the ISLP.models package. This takes

a model from statsmodels along with a search strategy and selects a model with its

fit method. Without specifying a scoring argument, the score defaults to MSE, and so all 19 variables will be

selected.

hitters_MSE = sklearn_selected(OLS, strategy)

hitters_MSE.fit(Hitters, Y)

hitters_MSE.selected_state_('Assists',

'AtBat',

'CAtBat',

'CHits',

'CHmRun',

'CRBI',

'CRuns',

'CWalks',

'Division',

'Errors',

'Hits',

'HmRun',

'League',

'NewLeague',

'PutOuts',

'RBI',

'Runs',

'Walks',

'Years')Using neg_Cp results in a smaller model, as expected, with just 10 variables selected.

hitters_Cp = sklearn_selected(OLS, strategy, scoring=neg_Cp)

hitters_Cp.fit(Hitters, Y)

hitters_Cp.selected_state_('Assists',

'AtBat',

'CAtBat',

'CRBI',

'CRuns',

'CWalks',

'Division',

'Hits',

'PutOuts',

'Walks')Choosing Among Models Using the Validation Set Approach and Cross-Validation¶

As an alternative to using , we might try cross-validation to select a model in forward selection. For this, we need a

method that stores the full path of models found in forward selection, and allows predictions for each of these. This can be done with the sklearn_selection_path()

estimator from ISLP.models. The function cross_val_predict() from ISLP.models

computes the cross-validated predictions for each of the models

along the path, which we can use to evaluate the cross-validated MSE

along the path.

Here we define a strategy that fits the full forward selection path.

While there are various parameter choices for sklearn_selection_path(),

we use the defaults here, which selects the model at each step based on the biggest reduction in RSS.

strategy = Stepwise.fixed_steps(design, len(design.terms), direction="forward")

full_path = sklearn_selection_path(OLS, strategy)We now fit the full forward-selection path on the Hitters data and compute the fitted values.

full_path.fit(Hitters, Y)

Yhat_in = full_path.predict(Hitters)

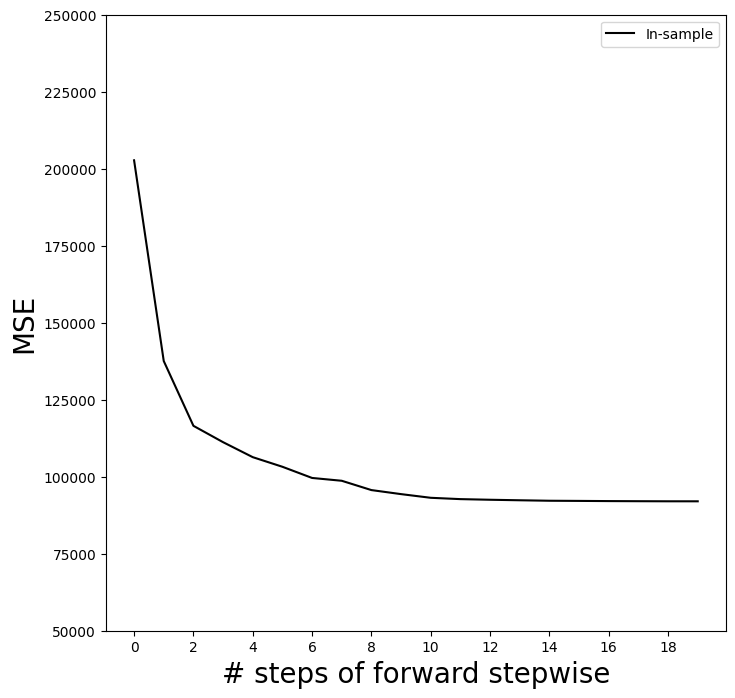

Yhat_in.shape(263, 20)This gives us an array of fitted values --- 20 steps in all, including the fitted mean for the null model --- which we can use to evaluate in-sample MSE. As expected, the in-sample MSE improves each step we take, indicating we must use either the validation or cross-validation approach to select the number of steps. We fix the y-axis to range from 50,000 to 250,000 to compare to the cross-validation and validation set MSE below, as well as other methods such as ridge regression, lasso and principal components regression.

mse_fig, ax = subplots(figsize=(8, 8))

insample_mse = ((Yhat_in - Y[:, None]) ** 2).mean(0)

n_steps = insample_mse.shape[0]

ax.plot(

np.arange(n_steps),

insample_mse,

"k", # color black

label="In-sample",

)

ax.set_ylabel("MSE", fontsize=20)

ax.set_xlabel("# steps of forward stepwise", fontsize=20)

ax.set_xticks(np.arange(n_steps)[::2])

ax.legend()

ax.set_ylim([50000, 250000]);

Notice the expression None in Y[:,None] above.

This adds an axis (dimension) to the one-dimensional array Y,

which allows it to be recycled when subtracted from the two-dimensional Yhat_in.

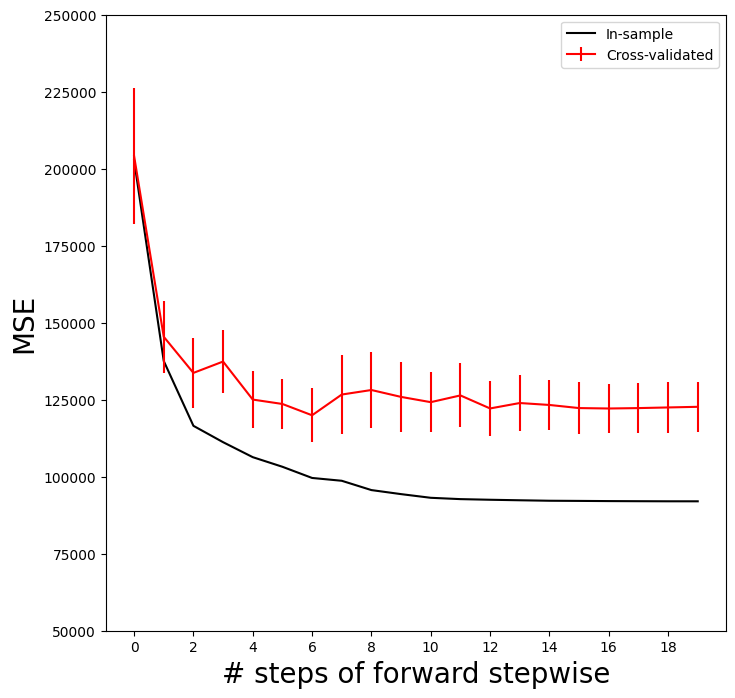

We are now ready to use cross-validation to estimate test error along the model path. We must use only the training observations to perform all aspects of model-fitting --- including variable selection. Therefore, the determination of which model of a given size is best must be made using \emph{only the training observations} in each training fold. This point is subtle but important. If the full data set is used to select the best subset at each step, then the validation set errors and cross-validation errors that we obtain will not be accurate estimates of the test error.

We now compute the cross-validated predicted values using 5-fold cross-validation.

K = 5

kfold = skm.KFold(K, random_state=0, shuffle=True)

Yhat_cv = skm.cross_val_predict(full_path, Hitters, Y, cv=kfold)

Yhat_cv.shape(263, 20)skm.cross_val_predict()

The prediction matrix Yhat_cv is the same shape as Yhat_in; the difference is that the predictions in each row, corresponding to a particular sample index, were made from models fit on a training fold that did not include that row.

At each model along the path, we compute the MSE in each of the cross-validation folds.

These we will average to get the mean MSE, and can also use the individual values to compute a crude estimate of the standard error of the mean. {The estimate is crude because the five error estimates are based on overlapping training sets, and hence are not independent.}

Hence we must know the test indices for each cross-validation

split. This can be found by using the split() method of kfold. Because

we fixed the random state above, whenever we split any array with the same

number of rows as we recover the same training and test indices, though we simply

ignore the training indices below.

cv_mse = []

for train_idx, test_idx in kfold.split(Y):

errors = (Yhat_cv[test_idx] - Y[test_idx, None]) ** 2

cv_mse.append(errors.mean(0)) # column means

cv_mse = np.array(cv_mse).T

cv_mse.shape(20, 5)We now add the cross-validation error estimates to our MSE plot. We include the mean error across the five folds, and the estimate of the standard error of the mean.

ax.errorbar(

np.arange(n_steps),

cv_mse.mean(1),

cv_mse.std(1) / np.sqrt(K),

label="Cross-validated",

c="r",

) # color red

ax.set_ylim([50000, 250000])

ax.legend()

mse_fig

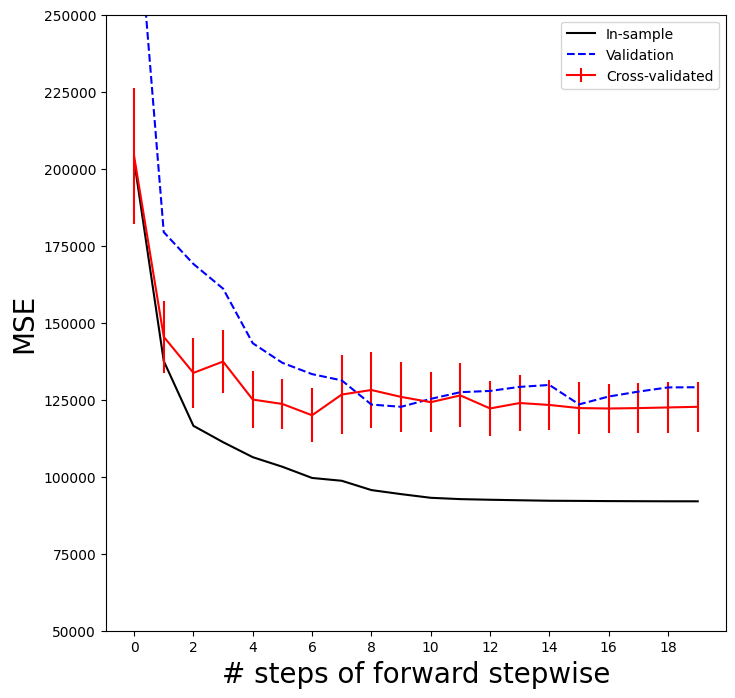

To repeat the above using the validation set approach, we simply change our

cv argument to a validation set: one random split of the data into a test and training. We choose a test size

of 20%, similar to the size of each test set in 5-fold cross-validation.skm.ShuffleSplit()

validation = skm.ShuffleSplit(n_splits=1, test_size=0.2, random_state=0)

for train_idx, test_idx in validation.split(Y):

full_path.fit(Hitters.iloc[train_idx], Y[train_idx])

Yhat_val = full_path.predict(Hitters.iloc[test_idx])

errors = (Yhat_val - Y[test_idx, None]) ** 2

validation_mse = errors.mean(0)As for the in-sample MSE case, the validation set approach does not provide standard errors.

ax.plot(

np.arange(n_steps),

validation_mse,

"b--", # color blue, broken line

label="Validation",

)

ax.set_xticks(np.arange(n_steps)[::2])

ax.set_ylim([50000, 250000])

ax.legend()

mse_fig

Best Subset Selection¶

Forward stepwise is a greedy selection procedure; at each step it augments the current set by including one additional variable. We now apply best subset selection to the Hitters

data, which for every subset size, searches for the best set of predictors.

We will use a package called l0bnb to perform

best subset selection.

Instead of constraining the subset to be a given size,

this package produces a path of solutions using the subset size as a

penalty rather than a constraint. Although the distinction is subtle, the difference comes when we cross-validate.

D = design.fit_transform(Hitters)

D = D.drop("intercept", axis=1)

X = np.asarray(D)Here we excluded the first column corresponding to the intercept, as

l0bnb will fit the intercept separately. We can find a path using the fit_path() function.

path = fit_path(X, Y, max_nonzeros=X.shape[1])Preprocessing Data.

BnB Started.

Iteration: 1. Number of non-zeros: 1

Iteration: 2. Number of non-zeros: 2

Iteration: 3. Number of non-zeros: 2

Iteration: 4. Number of non-zeros: 2

Iteration: 5. Number of non-zeros: 3

Iteration: 6. Number of non-zeros: 3

Iteration: 7. Number of non-zeros: 4

Iteration: 8. Number of non-zeros: 9

Iteration: 9. Number of non-zeros: 9

Iteration: 10. Number of non-zeros: 9

Iteration: 11. Number of non-zeros: 9

Iteration: 12. Number of non-zeros: 9

Iteration: 13. Number of non-zeros: 9

Iteration: 14. Number of non-zeros: 9

Iteration: 15. Number of non-zeros: 9

Iteration: 16. Number of non-zeros: 9

Iteration: 17. Number of non-zeros: 9

Iteration: 18. Number of non-zeros: 17

Iteration: 19. Number of non-zeros: 19

The function fit_path() returns a list whose values include the fitted coefficients as B, an intercept as B0, as well as a few other attributes related to the particular path algorithm used. Such details are beyond the scope of this book.

path[3]{'B': array([0. , 3.25484367, 0. , 0. , 0. ,

0. , 0. , 0. , 0. , 0. ,

0. , 0.67775265, 0. , 0. , 0. ,

0. , 0. , 0. , 0. ]),

'B0': -38.98216739555551,

'lambda_0': 0.011416248027450178,

'M': 0.5829861733382012,

'Time_exceeded': False}In the example above, we see that at the fourth step in the path, we have two nonzero coefficients in 'B', corresponding to the value 0.114 for the penalty parameter lambda_0.

We could make predictions using this sequence of fits on a validation set as a function of lambda_0, or with more work using cross-validation.

Ridge Regression and the Lasso¶

We will use the sklearn.linear_model package (for which

we use skl as shorthand below)

to fit ridge and lasso regularized linear models on the Hitters data.

We start with the model matrix X (without an intercept) that we computed in the previous section on best subset regression.

Ridge Regression¶

We will use the function skl.ElasticNet() to fit both ridge and the lasso.

To fit a path of ridge regressions models, we use

skl.ElasticNet.path(), which can fit both ridge and lasso, as well as a hybrid mixture; ridge regression

corresponds to l1_ratio=0.

It is good practice to standardize the columns of X in these applications, if the variables are measured in different units. Since skl.ElasticNet() does no normalization, we have to take care of that ourselves.

Since we

standardize first, in order to find coefficient

estimates on the original scale, we must unstandardize

the coefficient estimates. The parameter

λ in (\ref{Ch6:ridge}) and (\ref{Ch6:LASSO}) is called alphas in sklearn. In order to

be consistent with the rest of this chapter, we use lambdas

rather than alphas in what follows. {At the time of publication, ridge fits like the one in code chunk [22] issue unwarranted convergence warning messages; we expect these to disappear as this package matures.}

Xs = X - X.mean(0)[None, :]

X_scale = X.std(0)

Xs = Xs / X_scale[None, :]

lambdas = 10 ** np.linspace(8, -2, 100) / Y.std()

soln_array = skl.ElasticNet.path(Xs, Y, l1_ratio=0.0, alphas=lambdas)[1]

soln_array.shape(19, 100)Here we extract the array of coefficients corresponding to the solutions along the regularization path.

By default the skl.ElasticNet.path method fits a path along

an automatically selected range of λ values, except for the case when

l1_ratio=0, which results in ridge regression (as is the case here). {The reason is rather technical; for all models except ridge, we can find the smallest value of λ for which all coefficients are zero. For ridge this value is ∞.} So here

we have chosen to implement the function over a grid of values ranging

from to scaled by the standard

deviation of , essentially covering the full range of scenarios

from the null model containing only the intercept, to the least

squares fit.

Associated with each value of λ is a vector of ridge

regression coefficients, that can be accessed by

a column of soln_array. In this case, soln_array is a matrix, with

19 rows (one for each predictor) and 100

columns (one for each value of λ).

We transpose this matrix and turn it into a data frame to facilitate viewing and plotting.

soln_path = pd.DataFrame(soln_array.T, columns=D.columns, index=-np.log(lambdas))

soln_path.index.name = "negative log(lambda)"

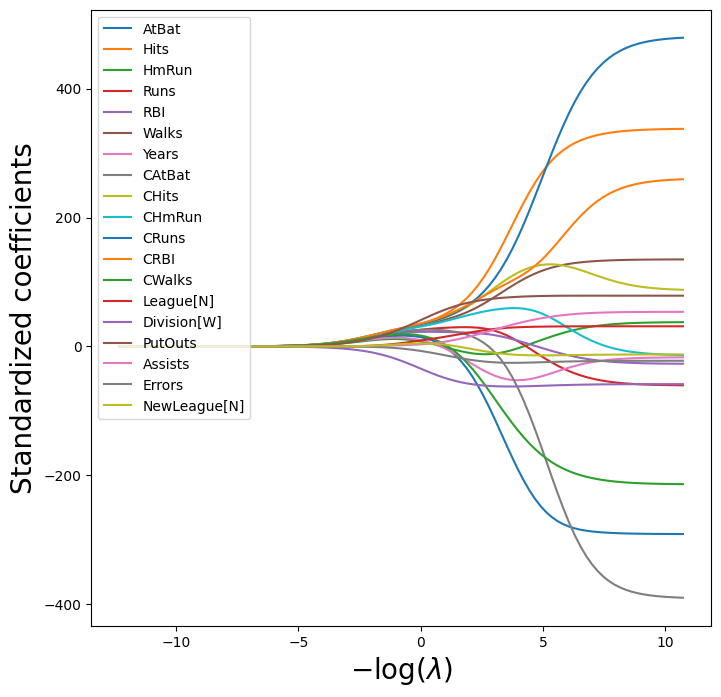

soln_pathWe plot the paths to get a sense of how the coefficients vary with λ.

To control the location of the legend we first set legend to False in the

plot method, adding it afterward with the legend() method of ax.

path_fig, ax = subplots(figsize=(8, 8))

soln_path.plot(ax=ax, legend=False)

ax.set_xlabel(r"$-\log(\lambda)$", fontsize=20)

ax.set_ylabel("Standardized coefficients", fontsize=20)

ax.legend(loc="upper left");

(We have used latex formatting in the horizontal label, in order to format the Greek λ appropriately.)

We expect the coefficient estimates to be much smaller, in terms of

norm, when a large value of λ is used, as compared to

when a small value of λ is used. (Recall that the norm is the square root of the sum of squared coefficient values.) We display the coefficients at the 40th step,

where λ is 25.535.

beta_hat = soln_path.loc[soln_path.index[39]]

lambdas[39], beta_hat(25.53538897200662,

AtBat 5.433750

Hits 6.223582

HmRun 4.585498

Runs 5.880855

RBI 6.195921

Walks 6.277975

Years 5.299767

CAtBat 7.147501

CHits 7.539495

CHmRun 7.182344

CRuns 7.728649

CRBI 7.790702

CWalks 6.592901

League[N] 0.042445

Division[W] -3.107159

PutOuts 4.605263

Assists 0.378371

Errors -0.135196

NewLeague[N] 0.150323

Name: -3.240065292879872, dtype: float64)Let’s compute the norm of the standardized coefficients.

np.linalg.norm(beta_hat)24.17061720144378In contrast, here is the norm when λ is 2.44e-01. Note the much larger norm of the coefficients associated with this smaller value of λ.

beta_hat = soln_path.loc[soln_path.index[59]]

lambdas[59], np.linalg.norm(beta_hat)(0.24374766133488554, 160.42371017725839)Above we normalized X upfront, and fit the ridge model using Xs.

The Pipeline() object

in sklearn provides a clear way to separate feature

normalization from the fitting of the ridge model itself.

ridge = skl.ElasticNet(alpha=lambdas[59], l1_ratio=0)

scaler = StandardScaler(with_mean=True, with_std=True)

pipe = Pipeline(steps=[("scaler", scaler), ("ridge", ridge)])

pipe.fit(X, Y)We show that it gives the same norm as in our previous fit on the standardized data.

np.linalg.norm(ridge.coef_)160.4237101772591Notice that the operation pipe.fit(X, Y) above has changed the ridge object, and in particular has added attributes such as coef_ that were not there before.

Estimating Test Error of Ridge Regression¶

Choosing an a priori value of λ for ridge regression is

difficult if not impossible. We will want to use the validation method

or cross-validation to select the tuning parameter. The reader may not

be surprised that the Pipeline() approach can be used in

skm.cross_validate() with either a validation method

(i.e. validation) or -fold cross-validation.

We fix the random state of the splitter so that the results obtained will be reproducible.

validation = skm.ShuffleSplit(n_splits=1, test_size=0.5, random_state=0)

ridge.alpha = 0.01

results = skm.cross_validate(

ridge,

X,

Y,

scoring="neg_mean_squared_error",

cv=validation,

)

-results["test_score"]array([134214.00419204])The test MSE is 1.342e+05. Note

that if we had instead simply fit a model with just an intercept, we

would have predicted each test observation using the mean of the

training observations. We can get the same result by fitting a ridge regression model

with a very large value of λ. Note that 1e10

means 1010.

ridge.alpha = 1e10

results = skm.cross_validate(

ridge,

X,

Y,

scoring="neg_mean_squared_error",

cv=validation,

)

-results["test_score"]array([231788.32155285])Obviously choosing is arbitrary, so we will use cross-validation or the validation-set

approach to choose the tuning parameter λ.

The object GridSearchCV() allows exhaustive

grid search to choose such a parameter.

We first use the validation set method to choose λ.

param_grid = {"ridge__alpha": lambdas}

grid = skm.GridSearchCV(

pipe,

param_grid,

cv=validation,

scoring="neg_mean_squared_error",

)

grid.fit(X, Y)

grid.best_params_["ridge__alpha"]

grid.best_estimator_Alternatively, we can use 5-fold cross-validation.

grid = skm.GridSearchCV(pipe, param_grid, cv=kfold, scoring="neg_mean_squared_error")

grid.fit(X, Y)

grid.best_params_["ridge__alpha"]

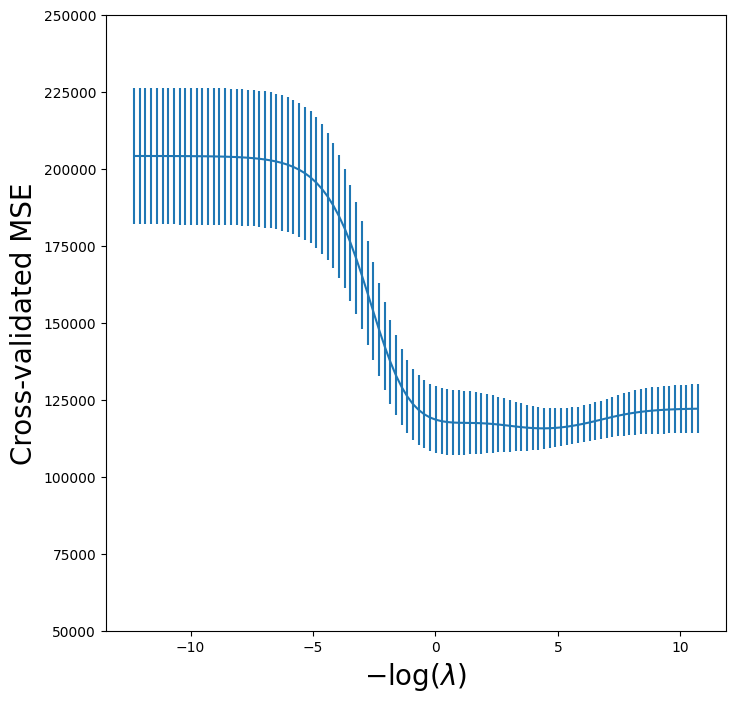

grid.best_estimator_Recall we set up the kfold object for 5-fold cross-validation on page~\pageref{line:choos-among-models}. We now plot the cross-validated MSE as a function of , which has shrinkage decreasing from left

to right.

ridge_fig, ax = subplots(figsize=(8, 8))

ax.errorbar(

-np.log(lambdas),

-grid.cv_results_["mean_test_score"],

yerr=grid.cv_results_["std_test_score"] / np.sqrt(K),

)

ax.set_ylim([50000, 250000])

ax.set_xlabel(r"$-\log(\lambda)$", fontsize=20)

ax.set_ylabel("Cross-validated MSE", fontsize=20);

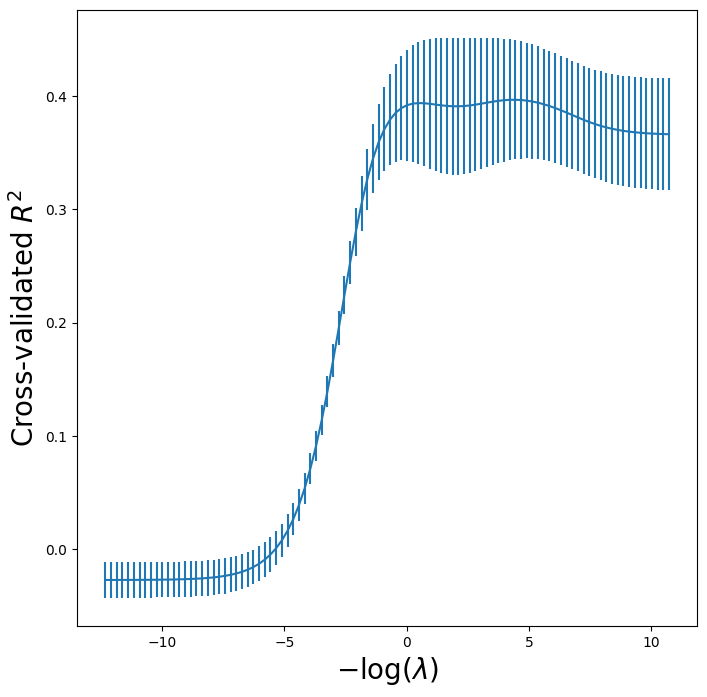

One can cross-validate different metrics to choose a parameter. The default

metric for skl.ElasticNet() is test .

Let’s compare to MSE for cross-validation here.

grid_r2 = skm.GridSearchCV(pipe, param_grid, cv=kfold)

grid_r2.fit(X, Y)Finally, let’s plot the results for cross-validated .

r2_fig, ax = subplots(figsize=(8, 8))

ax.errorbar(

-np.log(lambdas),

grid_r2.cv_results_["mean_test_score"],

yerr=grid_r2.cv_results_["std_test_score"] / np.sqrt(K),

)

ax.set_xlabel(r"$-\log(\lambda)$", fontsize=20)

ax.set_ylabel("Cross-validated $R^2$", fontsize=20);

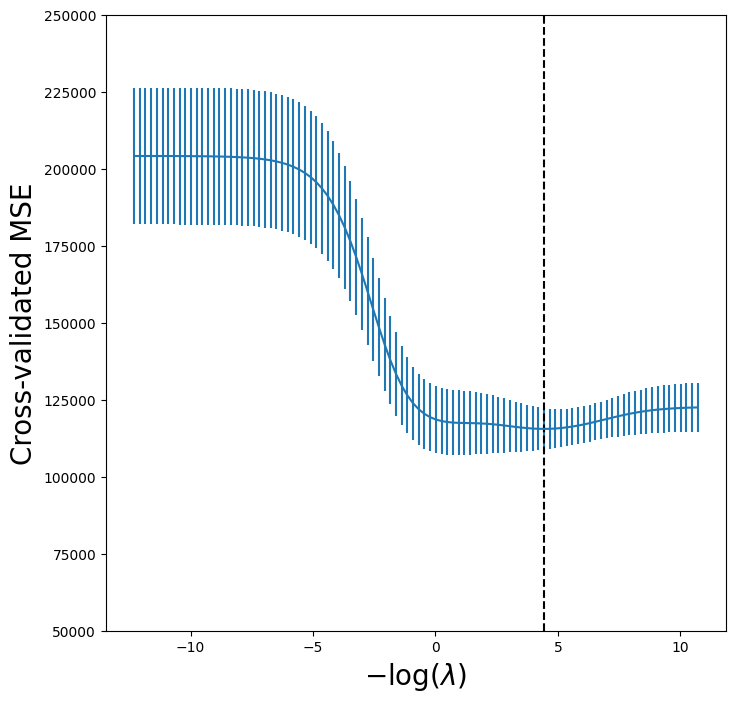

Fast Cross-Validation for Solution Paths¶

The ridge, lasso, and elastic net can be efficiently fit along a sequence of λ values, creating what is known as a solution path or regularization path. Hence there is specialized code to fit

such paths, and to choose a suitable value of λ using cross-validation. Even with

identical splits the results will not agree exactly with our grid

above because the standardization of each feature in grid is carried out on each fold,

while in pipeCV below it is carried out only once.

Nevertheless, the results are similar as the normalization

is relatively stable across folds.

ridgeCV = skl.ElasticNetCV(alphas=lambdas, l1_ratio=0, cv=kfold)

pipeCV = Pipeline(steps=[("scaler", scaler), ("ridge", ridgeCV)])

pipeCV.fit(X, Y)Let’s produce a plot again of the cross-validation error to see that

it is similar to using skm.GridSearchCV.

tuned_ridge = pipeCV.named_steps["ridge"]

ridgeCV_fig, ax = subplots(figsize=(8, 8))

ax.errorbar(

-np.log(lambdas),

tuned_ridge.mse_path_.mean(1),

yerr=tuned_ridge.mse_path_.std(1) / np.sqrt(K),

)

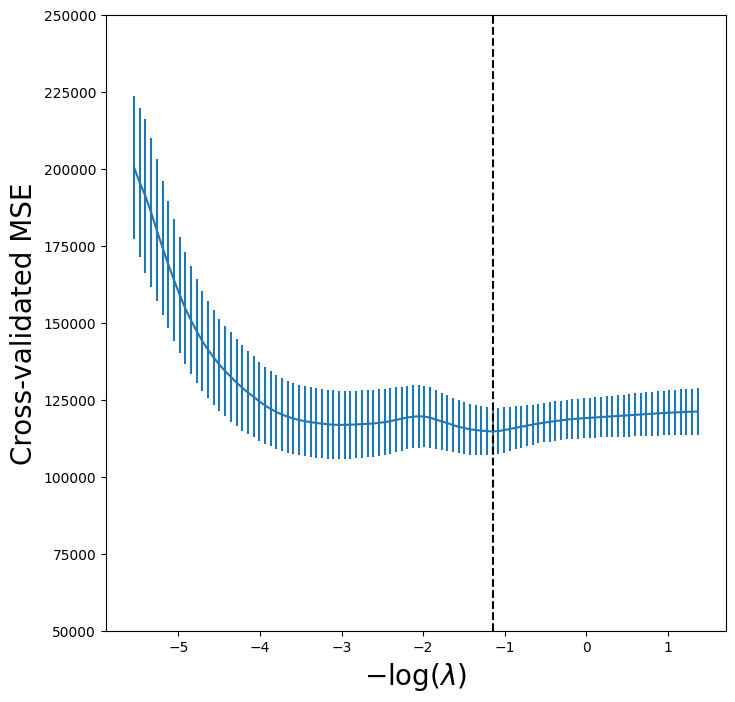

ax.axvline(-np.log(tuned_ridge.alpha_), c="k", ls="--")

ax.set_ylim([50000, 250000])

ax.set_xlabel(r"$-\log(\lambda)$", fontsize=20)

ax.set_ylabel("Cross-validated MSE", fontsize=20);

We see that the value of λ that results in the

smallest cross-validation error is 1.19e-02, available

as the value tuned_ridge.alpha_. What is the test MSE

associated with this value of λ?

np.min(tuned_ridge.mse_path_.mean(1))115526.70630987917This represents a further improvement over the test MSE that we got

using . Finally, tuned_ridge.coef_

has the coefficients fit on the entire data set

at this value of λ.

tuned_ridge.coef_array([-222.80877051, 238.77246614, 3.21103754, -2.93050845,

3.64888723, 108.90953869, -50.81896152, -105.15731984,

122.00714801, 57.1859509 , 210.35170348, 118.05683748,

-150.21959435, 30.36634231, -61.62459095, 77.73832472,

40.07350744, -25.02151514, -13.68429544])As expected, none of the coefficients are zero—ridge regression does not perform variable selection!

Evaluating Test Error of Cross-Validated Ridge¶

Choosing λ using cross-validation provides a single regression estimator, similar to fitting a linear regression model as we saw in Chapter~\ref{Ch3:linreg}. It is therefore reasonable to estimate what its test error is. We run into a problem here in that cross-validation will have touched all of its data in choosing λ, hence we have no further data to estimate test error. A compromise is to do an initial split of the data into two disjoint sets: a training set and a test set. We then fit a cross-validation tuned ridge regression on the training set, and evaluate its performance on the test set. We might call this cross-validation nested within the validation set approach. A priori there is no reason to use half of the data for each of the two sets in validation. Below, we use 75% for training and 25% for test, with the estimator being ridge regression tuned using 5-fold cross-validation. This can be achieved in code as follows:

outer_valid = skm.ShuffleSplit(n_splits=1, test_size=0.25, random_state=1)

inner_cv = skm.KFold(n_splits=5, shuffle=True, random_state=2)

ridgeCV = skl.ElasticNetCV(alphas=lambdas, l1_ratio=0, cv=inner_cv)

pipeCV = Pipeline(steps=[("scaler", scaler), ("ridge", ridgeCV)]);results = skm.cross_validate(

pipeCV,

X,

Y,

cv=outer_valid,

scoring="neg_mean_squared_error",

)

-results["test_score"]array([132393.84003227])The Lasso¶

We saw that ridge regression with a wise choice of λ can

outperform least squares as well as the null model on the

Hitters data set. We now ask whether the lasso can yield

either a more accurate or a more interpretable model than ridge

regression. In order to fit a lasso model, we once again use the

ElasticNetCV() function; however, this time we use the argument

l1_ratio=1. Other than that change, we proceed just as we did in

fitting a ridge model.

lassoCV = skl.ElasticNetCV(n_alphas=100, l1_ratio=1, cv=kfold)

pipeCV = Pipeline(steps=[("scaler", scaler), ("lasso", lassoCV)])

pipeCV.fit(X, Y)

tuned_lasso = pipeCV.named_steps["lasso"]

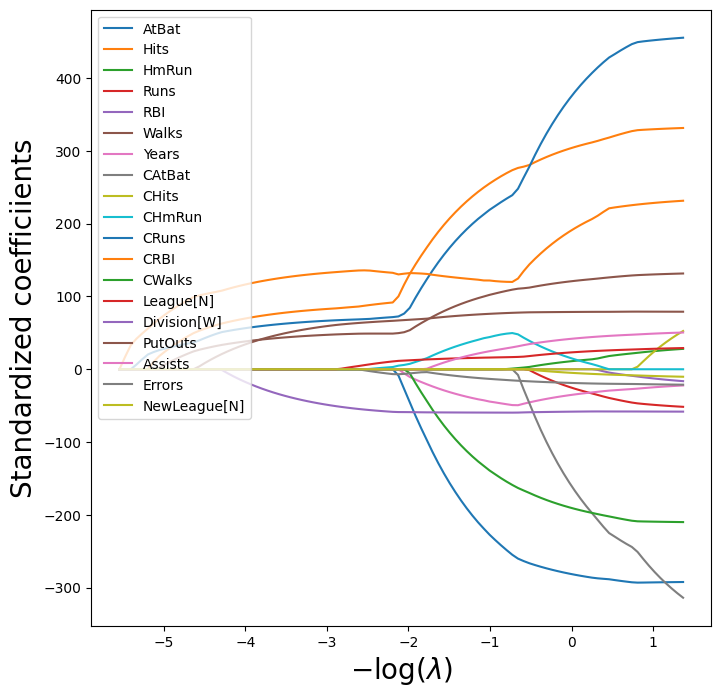

tuned_lasso.alpha_3.1472370031649866lambdas, soln_array = skl.Lasso.path(Xs, Y, l1_ratio=1, n_alphas=100)[:2]

soln_path = pd.DataFrame(soln_array.T, columns=D.columns, index=-np.log(lambdas))We can see from the coefficient plot of the standardized coefficients that depending on the choice of tuning parameter, some of the coefficients will be exactly equal to zero.

path_fig, ax = subplots(figsize=(8, 8))

soln_path.plot(ax=ax, legend=False)

ax.legend(loc="upper left")

ax.set_xlabel(r"$-\log(\lambda)$", fontsize=20)

ax.set_ylabel("Standardized coefficiients", fontsize=20);

The smallest cross-validated error is lower than the test set MSE of the null model and of least squares, and very similar to the test MSE of 115526.71 of ridge regression (page~\pageref{page:MSECVRidge}) with λ chosen by cross-validation.

np.min(tuned_lasso.mse_path_.mean(1))114690.73118253727Let’s again produce a plot of the cross-validation error.

lassoCV_fig, ax = subplots(figsize=(8, 8))

ax.errorbar(

-np.log(tuned_lasso.alphas_),

tuned_lasso.mse_path_.mean(1),

yerr=tuned_lasso.mse_path_.std(1) / np.sqrt(K),

)

ax.axvline(-np.log(tuned_lasso.alpha_), c="k", ls="--")

ax.set_ylim([50000, 250000])

ax.set_xlabel(r"$-\log(\lambda)$", fontsize=20)

ax.set_ylabel("Cross-validated MSE", fontsize=20);

However, the lasso has a substantial advantage over ridge regression in that the resulting coefficient estimates are sparse. Here we see that 6 of the 19 coefficient estimates are exactly zero. So the lasso model with λ chosen by cross-validation contains only 13 variables.

tuned_lasso.coef_array([-210.01008773, 243.4550306 , 0. , 0. ,

0. , 97.69397357, -41.52283116, -0. ,

0. , 39.62298193, 205.75273856, 124.55456561,

-126.29986768, 15.70262427, -59.50157967, 75.24590036,

21.62698014, -12.04423675, -0. ])As in ridge regression, we could evaluate the test error of cross-validated lasso by first splitting into test and training sets and internally running cross-validation on the training set. We leave this as an exercise.

PCR and PLS Regression¶

Principal Components Regression¶

Principal components regression (PCR) can be performed using

PCA() from the sklearn.decomposition

module. We now apply PCR to the Hitters data, in order to

predict Salary. Again, ensure that the missing values have

been removed from the data, as described in Section~\ref{Ch6-varselect-lab:lab-1-subset-selection-methods}.

We use LinearRegression() to fit the regression model

here. Note that it fits an intercept by default, unlike

the OLS() function seen earlier in Section~\ref{Ch6-varselect-lab:lab-1-subset-selection-methods}.

pca = PCA(n_components=2)

linreg = skl.LinearRegression()

pipe = Pipeline([("pca", pca), ("linreg", linreg)])

pipe.fit(X, Y)

pipe.named_steps["linreg"].coef_array([0.09846131, 0.4758765 ])When performing PCA, the results vary depending on whether the data has been standardized or not. As in the earlier examples, this can be accomplished by including an additional step in the pipeline.

pipe = Pipeline([("scaler", scaler), ("pca", pca), ("linreg", linreg)])

pipe.fit(X, Y)

pipe.named_steps["linreg"].coef_array([106.36859204, 21.60350456])We can of course use CV to choose the number of components, by

using skm.GridSearchCV, in this

case fixing the parameters to vary the

n_components.

param_grid = {"pca__n_components": range(1, 20)}

grid = skm.GridSearchCV(pipe, param_grid, cv=kfold, scoring="neg_mean_squared_error")

grid.fit(X, Y)Let’s plot the results as we have for other methods.

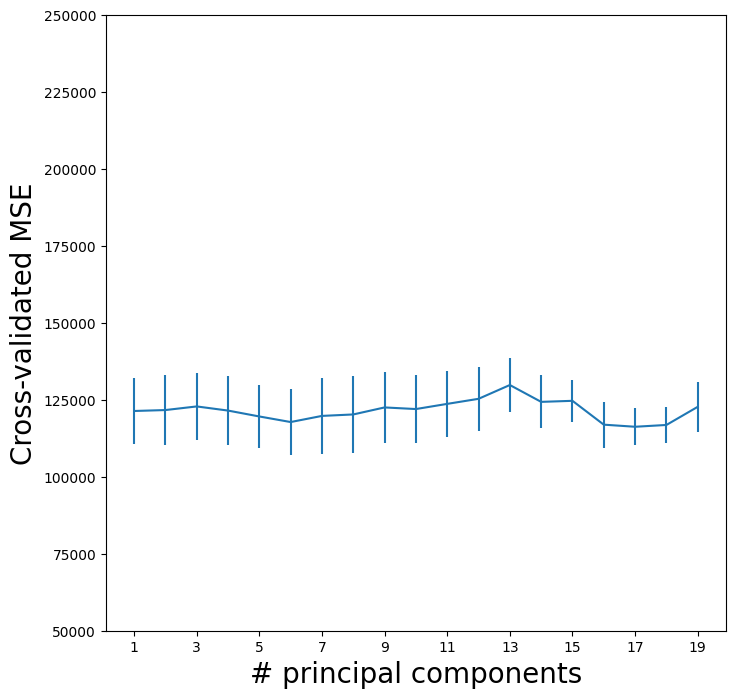

pcr_fig, ax = subplots(figsize=(8, 8))

n_comp = param_grid["pca__n_components"]

ax.errorbar(

n_comp,

-grid.cv_results_["mean_test_score"],

grid.cv_results_["std_test_score"] / np.sqrt(K),

)

ax.set_ylabel("Cross-validated MSE", fontsize=20)

ax.set_xlabel("# principal components", fontsize=20)

ax.set_xticks(n_comp[::2])

ax.set_ylim([50000, 250000]);

We see that the smallest cross-validation error occurs when 17 components are used. However, from the plot we also see that the cross-validation error is roughly the same when only one component is included in the model. This suggests that a model that uses just a small number of components might suffice.

The CV score is provided for each possible number of components from

1 to 19 inclusive. The PCA() method complains

if we try to fit an intercept only with n_components=0

so we also compute the MSE for just the null model with

these splits.

Xn = np.zeros((X.shape[0], 1))

cv_null = skm.cross_validate(linreg, Xn, Y, cv=kfold, scoring="neg_mean_squared_error")

-cv_null["test_score"].mean()204139.30692994667The explained_variance_ratio_

attribute of our PCA object provides the percentage of variance explained in the predictors and in the response using

different numbers of components. This concept is discussed in greater

detail in Section~\ref{Ch10:sec:pca}.

pipe.named_steps["pca"].explained_variance_ratio_array([0.3831424 , 0.21841076])Briefly, we can think of this as the amount of information about the predictors that is captured using principal components. For example, setting only captures 38.31% of the variance, while captures an additional 21.84%, for a total of 60.15% of the variance. By it increases to 88.63%. Beyond this the increments continue to diminish, until we use all components, which captures all 100% of the variance.

Partial Least Squares¶

Partial least squares (PLS) is implemented in the

PLSRegression() function.

pls = PLSRegression(n_components=2, scale=True)

pls.fit(X, Y)As was the case in PCR, we will want to use CV to choose the number of components.

param_grid = {"n_components": range(1, 20)}

grid = skm.GridSearchCV(pls, param_grid, cv=kfold, scoring="neg_mean_squared_error")

grid.fit(X, Y)As for our other methods, we plot the MSE.

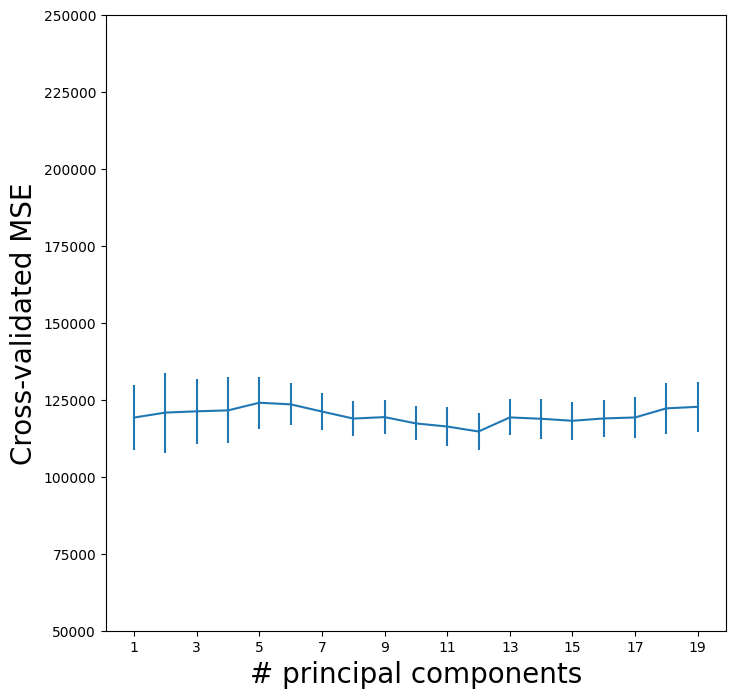

pls_fig, ax = subplots(figsize=(8, 8))

n_comp = param_grid["n_components"]

ax.errorbar(

n_comp,

-grid.cv_results_["mean_test_score"],

grid.cv_results_["std_test_score"] / np.sqrt(K),

)

ax.set_ylabel("Cross-validated MSE", fontsize=20)

ax.set_xlabel("# principal components", fontsize=20)

ax.set_xticks(n_comp[::2])

ax.set_ylim([50000, 250000]);

CV error is minimized at 12, though there is little noticable difference between this point and a much lower number like 2 or 3 components.