Learning Objectives

Upon completion of this chapter, readers will demonstrate proficiency in advanced regression modeling using Python by:

6.1 Implementing logarithmic transformations of variables using NumPy log functions and interpreting semi-elasticities and elasticities from regression output.

6.2 Estimating models with quadratic terms and computing turning points through coefficient manipulation and calculus in Python.

6.3 Creating and interpreting interaction terms between continuous and categorical variables using patsy formulas and pandas operations.

6.4 Computing standardized regression coefficients through z-score normalization with pandas and NumPy for comparing effect magnitudes.

6.5 Generating prediction intervals using statsmodels get_prediction method with confidence bands for out-of-sample forecasting.

6.6 Implementing adjusted R-squared calculations and conducting model comparison using information criteria (AIC, BIC) from statsmodels.

6.7 Visualizing nonlinear relationships and interactions through conditional effect plots using seaborn and matplotlib.

6.8 Automating functional form testing including quadratic specification tests and interaction significance assessment.

Advanced applications of multiple regression require careful attention to model specification, functional form selection, and prediction methodology. This chapter extends foundational regression concepts to address practical challenges in empirical research: choosing appropriate transformations of variables, modeling interaction effects, incorporating quadratic relationships, and constructing prediction intervals that account for multiple sources of uncertainty.

The development proceeds hierarchically from data scaling considerations to sophisticated modeling techniques. We examine how changes in measurement units affect coefficient interpretation (Section 6.1), introduce logarithmic transformations for modeling percentage effects and elasticities (Section 6.2), develop methods for incorporating quadratic and interaction terms (Section 6.3), address challenges in standardized coefficients and goodness-of-fit measures (Section 6.4), and conclude with prediction theory and interval construction (Section 6.5-6.6). Throughout, we implement these methods using Python’s statsmodels library and illustrate applications with real datasets from econometric research.

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import statsmodels.formula.api as smf

import wooldridge as wool

from scipy import stats6.1 Model Formulae¶

This section explores how to use model formulae effectively to specify different types of regression models beyond the basic linear form. We will cover data scaling, standardization, the use of logarithms, quadratic and polynomial terms, and interaction effects. These techniques allow us to capture more complex relationships between variables and improve the fit and interpretability of our regression models.

6.1.1 Data Scaling: Arithmetic Operations within a Formula¶

Sometimes, the units in which variables are measured can affect the magnitude and interpretation of regression coefficients. Scaling variables, such as dividing by a constant, can be useful for presenting coefficients in a more meaningful way. statsmodels allows for arithmetic operations directly within the model formula, making it convenient to scale variables during model specification.

Consider the following model investigating the determinants of birth weight:

where:

bwghtis birth weight in ounces.cigsis the average number of cigarettes smoked per day by the mother during pregnancy.famincis family income.

We might want to express birth weight in pounds instead of ounces or cigarettes in packs per day instead of individual cigarettes. Let’s see how this can be done and how it affects the coefficients.

bwght = wool.data("bwght")

# regress and report coefficients:

reg = smf.ols(formula="bwght ~ cigs + faminc", data=bwght)

results = reg.fit()

# weight in pounds, manual way:

bwght["bwght_lbs"] = bwght["bwght"] / 16 # 1 pound = 16 ounces

reg_lbs = smf.ols(formula="bwght_lbs ~ cigs + faminc", data=bwght)

results_lbs = reg_lbs.fit()

# weight in pounds, direct way:

reg_lbs2 = smf.ols(

formula="I(bwght/16) ~ cigs + faminc",

data=bwght,

) # Use I() to perform arithmetic within formula

results_lbs2 = reg_lbs2.fit()

# packs of cigarettes:

reg_packs = smf.ols(

formula="bwght ~ I(cigs/20) + faminc",

data=bwght,

) # Assuming 20 cigarettes per pack

results_packs = reg_packs.fit()

# compare results:

table = pd.DataFrame(

{

"b": round(results.params, 4),

"b_lbs": round(results_lbs.params, 4),

"b_lbs2": round(results_lbs2.params, 4),

"b_packs": round(results_packs.params, 4),

},

)

tableInterpretation of Results:

b(bwght): This column shows the coefficients when birth weight is in ounces and cigarettes are in individual units. For example, the coefficient forcigsis approximately -0.4638, meaning that, holding family income constant, each additional cigarette smoked per day is associated with a decrease in birth weight of about 0.46 ounces.b_lbsandb_lbs2(bwght_lbs): These columns show the coefficients when birth weight is converted to pounds. Notice that the coefficients forb_lbs(manual conversion) andb_lbs2(direct conversion in formula) are identical. The coefficient forcigsis now approximately -0.0290. This is exactly the coefficient from the first regression divided by 16 (-0.4638 / 16 ~= -0.0290), as expected. An additional cigarette is now associated with a decrease of about 0.029 pounds in birth weight.b_packs(packs of cigs): Here, cigarettes are converted to packs (assuming 20 cigarettes per pack) within the formula. The coefficient forI(cigs/20)is approximately -9.2762. This is 20 times the coefficient from the first regression (-0.4638 * 20 ~= -9.276), as expected. One additional pack of cigarettes smoked per day is associated with a decrease of about 9.27 ounces in birth weight.

Key takeaway: Scaling the dependent or independent variables changes the scale of the corresponding regression coefficients but does not fundamentally alter the relationship being estimated. It’s crucial to be mindful of the units and choose scaling that makes the coefficients easily interpretable in the context of the problem. Using I() within the formula allows for convenient on-the-fly scaling.

6.1.2 Standardization: Beta Coefficients¶

Standardization involves transforming variables to have a mean of zero and a standard deviation of one. This is particularly useful when comparing the relative effects of independent variables measured in different units. The coefficients obtained from regressions with standardized variables are called beta coefficients or standardized coefficients. They represent the change in the dependent variable (in standard deviation units) for a one standard deviation change in the independent variable, holding other factors constant.

The standardization formula for a variable is:

where is the sample mean and is the sample standard deviation of .

Let’s revisit the housing price example and standardize some of the variables to obtain beta coefficients.

Example 6.1: Effects of Pollution on Housing Prices (Standardized Variables)¶

We consider a model to examine the effect of air pollution (nox, nitrogen oxide concentration) and other factors on housing prices (price). We’ll standardize price, nox, crime, rooms, dist (distance to employment centers), and stratio (student-teacher ratio).

where the _sc suffix denotes the standardized version of each variable.

# define a function for the standardization:

def scale(x):

x_mean = np.mean(x)

x_var = np.var(x, ddof=1) # ddof=1 for sample standard deviation (denominator n-1)

x_scaled = (x - x_mean) / np.sqrt(x_var)

return x_scaled

# standardize and estimate:

hprice2 = wool.data("hprice2")

hprice2["price_sc"] = scale(hprice2["price"])

hprice2["nox_sc"] = scale(hprice2["nox"])

hprice2["crime_sc"] = scale(hprice2["crime"])

hprice2["rooms_sc"] = scale(hprice2["rooms"])

hprice2["dist_sc"] = scale(hprice2["dist"])

hprice2["stratio_sc"] = scale(hprice2["stratio"])

reg = smf.ols(

formula="price_sc ~ 0 + nox_sc + crime_sc + rooms_sc + dist_sc + stratio_sc", # No constant needed after standardization if all variables are standardized

data=hprice2,

)

results = reg.fit()

# print regression table:

table = pd.DataFrame(

{

"b": round(results.params, 4),

"se": round(results.bse, 4),

"t": round(results.tvalues, 4),

"pval": round(results.pvalues, 4),

},

)

tableInterpretation of Beta Coefficients:

nox_sccoefficient (-0.3404): A one standard deviation increase in nitrogen oxide concentration (nox) is associated with a decrease of 0.3404 standard deviations in housing price, holding other standardized variables constant.rooms_sccoefficient (0.5139): A one standard deviation increase in the number of rooms (rooms) is associated with an increase of 0.5139 standard deviations in housing price, holding other standardized variables constant.

Comparing Effects:

By comparing the absolute values of the beta coefficients, we can get a sense of the relative importance of each independent variable in explaining the variation in the dependent variable. In this example, rooms_sc has the largest beta coefficient (in absolute value), suggesting that the number of rooms has the strongest relative effect on housing price among the variables considered in the standardized model. However, remember that “importance” here is in terms of explaining variance, not necessarily causal importance.

Note on Constant Term: When all variables (dependent and independent) are standardized and a constant is included in the regression, the constant will always be zero. Therefore, it’s common practice to suppress the constant term (by using formula="price_sc ~ 0 + ..." or formula="price_sc ~ -1 + ...") when working with standardized variables, as done in the example above.

6.1.3 Logarithms¶

Logarithmic transformations are frequently used in regression analysis for several reasons:

Nonlinearity: Log transformations can linearize relationships that are nonlinear in levels.

Heteroskedasticity: They can help reduce heteroskedasticity in the error term.

Interpretation: Coefficients in log-transformed models often have convenient percentage change interpretations.

Common log transformations include:

Log-level model: . Here, a one-unit change in is associated with approximately a percent change in . This approximation is accurate when is small (typically ); the exact percentage change is percent.

Level-log model: . Here, a 1% increase in is associated with approximately a unit change in . More precisely, the change in from increasing by factor (e.g., for 1%) is .

Log-log model: . Here, a 1% change in is associated with a percent change in . The coefficient is the elasticity of with respect to , and this interpretation is exact, not an approximation.

Let’s consider a log-log model for housing prices:

hprice2 = wool.data("hprice2")

reg = smf.ols(formula="np.log(price) ~ np.log(nox) + rooms", data=hprice2)

results = reg.fit()

# print regression table:

table = pd.DataFrame(

{

"b": round(results.params, 4),

"se": round(results.bse, 4),

"t": round(results.tvalues, 4),

"pval": round(results.pvalues, 4),

},

)

tableInterpretation of Log-Log Model Coefficients:

np.log(nox)coefficient (-0.7177): A 1% increase in nitrogen oxide concentration (nox) is associated with approximately a 0.7177% decrease in housing price, holding the number of rooms constant. This is interpreted as an elasticity: the elasticity of housing price with respect tonoxis approximately -0.72.roomscoefficient (0.3059): An increase of one room is associated with approximately a increase in housing price, holdingnoxconstant. This is interpreted using the log-level approximation.

When to use Log Transformations:

Consider using log transformations for variables that are positively skewed.

If you suspect percentage changes are more relevant than absolute changes in the relationship.

When dealing with variables that must be non-negative (like prices, income, quantities).

Log-log models are particularly useful for estimating elasticities.

6.1.4 Quadratics and Polynomials¶

To model nonlinear relationships, we can include quadratic, cubic, or higher-order polynomial terms of independent variables in the regression model. A quadratic regression model includes the square of an independent variable:

This allows for a U-shaped or inverted U-shaped relationship between and . The slope of the relationship between and is no longer constant but depends on the value of :

To find the turning point (minimum or maximum) of the quadratic relationship, we can set the derivative to zero and solve for :

Example 6.2: Effects of Pollution on Housing Prices with Quadratic Terms¶

Let’s extend our housing price model to include a quadratic term for rooms and dist to allow for potentially nonlinear effects:

# Load housing price data for quadratic specification

hprice2 = wool.data("hprice2")

# Dataset information

pd.DataFrame(

{

"Metric": ["Number of observations", "Number of variables"],

"Value": [hprice2.shape[0], hprice2.shape[1]],

},

)

# Room statistics

pd.DataFrame(

{

"Statistic": ["Mean", "Min", "Max"],

"Value": [

f"{hprice2['rooms'].mean():.2f}",

hprice2["rooms"].min(),

hprice2["rooms"].max(),

],

},

)

# Specify quadratic model to capture nonlinear effects

# I() protects arithmetic operations in formula notation

quadratic_model = smf.ols(

formula="np.log(price) ~ np.log(nox) + np.log(dist) + rooms + I(rooms**2) + stratio",

data=hprice2,

)

quadratic_results = quadratic_model.fit()

# Display results with enhanced formatting

coefficients_table = pd.DataFrame(

{

"Coefficient": quadratic_results.params.round(4),

"Std_Error": quadratic_results.bse.round(4),

"t_statistic": quadratic_results.tvalues.round(4),

"p_value": quadratic_results.pvalues.round(4),

"Sig": [

"***" if p < 0.01 else "**" if p < 0.05 else "*" if p < 0.1 else ""

for p in quadratic_results.pvalues

],

},

)

# QUADRATIC MODEL RESULTS

# Dependent Variable: log(price)

coefficients_table

# Model statistics

pd.DataFrame(

{

"Metric": ["R-squared", "Number of observations"],

"Value": [f"{quadratic_results.rsquared:.4f}", int(quadratic_results.nobs)],

},

)Interpretation of Quadratic Term:

roomscoefficient (-0.5451) andI(rooms**2)coefficient (0.0623): The negative coefficient onroomsand the positive coefficient onrooms**2suggest a U-shaped relationship betweenroomsand . Initially, as the number of rooms increases, housing price decreases at a decreasing rate. However, beyond a certain point, further increases in rooms lead to increases in price.

Precise Calculations for Quadratic Effects:

Turning point: rooms

Marginal effect at mean (6.28 rooms): log points per room

Since dependent variable is log(price), a one-room increase at the mean raises price by approximately 23.7%

Units: The coefficients have units of (log dollars)/(room) and (log dollars)/(room^2)

Finding the Turning Point for Rooms:

The turning point (in terms of rooms) can be calculated as:

This suggests that the relationship between rooms and reaches its maximum (within the range of rooms considered in the model) at approximately 4.38 rooms. It’s important to examine the data range to see if this turning point is within the realistic range of the independent variable.

Polynomials beyond Quadratics: Cubic or higher-order polynomials can be used to model even more complex nonlinearities, but they can also become harder to interpret and may lead to overfitting if too many terms are included without strong theoretical justification.

6.1.5 Hypothesis Testing with Nonlinear Terms¶

When we include nonlinear terms like quadratics or interactions, we often want to test hypotheses about the joint significance of these terms. For example, in the quadratic model above, we might want to test whether the quadratic term for rooms is jointly significant with the linear term for rooms. We can use the F-test for joint hypotheses in statsmodels to do this.

Let’s test the joint hypothesis that both the coefficient on rooms and the coefficient on rooms**2 are simultaneously zero in Example 6.2.

hprice2 = wool.data("hprice2")

n = hprice2.shape[0]

reg = smf.ols(

formula="np.log(price) ~ np.log(nox)+np.log(dist)+rooms+I(rooms**2)+stratio",

data=hprice2,

)

results = reg.fit()

# implemented F test for rooms:

hypotheses = [

"rooms = 0",

"I(rooms ** 2) = 0",

] # Define the null hypotheses for joint test

ftest = results.f_test(hypotheses) # Perform the F-test

fstat = ftest.statistic

fpval = ftest.pvalue

# F-test results

pd.DataFrame(

{

"Metric": ["F-statistic", "p-value"],

"Value": [f"{fstat:.4f}", f"{fpval:.4f}"],

},

)Interpretation of F-test:

The F-statistic is 110.42, and the p-value is very close to zero. Since the p-value is much smaller than conventional significance levels (e.g., 0.05 or 0.01), we reject the null hypothesis that both coefficients on rooms and rooms**2 are jointly zero. We conclude that the number of rooms, considering both its linear and quadratic terms, is jointly statistically significant in explaining housing prices in this model.

6.1.6 Interaction Terms¶

Interaction terms allow the effect of one independent variable on the dependent variable to depend on the level of another independent variable. A basic interaction model with two independent variables and includes their product term:

In this model:

is the partial effect of on when .

is the partial effect of on when .

captures the interaction effect. It tells us how the effect of on changes as changes (and vice versa).

The partial effect of on is given by:

Similarly, the partial effect of on is:

Example 6.3: Effects of Attendance on Final Exam Performance with Interaction¶

Consider a model where we want to see how attendance rate (atndrte) and prior GPA (priGPA) affect student performance on a standardized final exam (stndfnl). We might hypothesize that the effect of attendance on exam performance is stronger for students with higher prior GPAs. To test this, we can include an interaction term between atndrte and priGPA. We also include quadratic terms for priGPA and ACT score to account for potential nonlinear effects of these control variables.

# Load student attendance data

attend = wool.data("attend")

n = attend.shape[0]

# Examine key variables

# Dataset information

pd.DataFrame(

{

"Metric": ["Number of observations"],

"Value": [n],

},

)

# Summary statistics

summary_stats = pd.DataFrame(

{

"Variable": ["Attendance rate", "Prior GPA"],

"Mean": [f"{attend['atndrte'].mean():.1f}%", f"{attend['priGPA'].mean():.2f}"],

"Std Dev": [f"{attend['atndrte'].std():.1f}%", f"{attend['priGPA'].std():.2f}"],

},

)

summary_stats

# Specify model with interaction and quadratic terms

# atndrte*priGPA creates main effects + interaction automatically

interaction_model = smf.ols(

formula="stndfnl ~ atndrte*priGPA + ACT + I(priGPA**2) + I(ACT**2)",

data=attend,

)

interaction_results = interaction_model.fit()

# Create comprehensive results table

results_table = pd.DataFrame(

{

"Coefficient": interaction_results.params.round(4),

"Std_Error": interaction_results.bse.round(4),

"t_statistic": interaction_results.tvalues.round(4),

"p_value": interaction_results.pvalues.round(4),

"Variable_Type": [

"Intercept",

"Main Effect", # atndrte

"Main Effect", # priGPA

"Control", # ACT

"Quadratic", # priGPA^2

"Quadratic", # ACT^2

"Interaction", # atndrtexpriGPA

],

},

)

# INTERACTION MODEL RESULTS

# Dependent Variable: stndfnl (Standardized Final Exam Score)

results_table

# Model statistics with interaction

pd.DataFrame(

{

"Metric": ["R-squared", "Adjusted R-squared"],

"Value": [

f"{interaction_results.rsquared:.4f}",

f"{interaction_results.rsquared_adj:.4f}",

],

},

)Interpretation of Interaction Term:

atndrte:priGPAcoefficient (0.0101): This positive coefficient suggests that the effect of attendance rate on final exam score increases as prior GPA increases. In other words, attendance seems to be more beneficial for students with higher prior GPAs.

Calculating Partial Effect of Attendance at a Specific priGPA:

Let’s calculate the estimated partial effect of attendance rate on stndfnl for a student with a prior GPA of 2.59 (the sample average of priGPA):

# Calculate partial effect of attendance at specific GPA values

# dstndfnl/datndrte = beta_1 + beta_6*priGPA

# Extract coefficients

coefficients = interaction_results.params

mean_priGPA = attend["priGPA"].mean() # Sample average GPA

# Calculate partial effect at mean GPA

partial_effect_at_mean = (

coefficients["atndrte"] + mean_priGPA * coefficients["atndrte:priGPA"]

)

# PARTIAL EFFECT ANALYSIS

# Partial effect calculation

pd.DataFrame(

{

"Component": [

"Base effect of attendance",

"Interaction at mean GPA",

"Total partial effect",

],

"Value": [

f"{coefficients['atndrte']:.4f}",

f"{mean_priGPA:.2f} x {coefficients['atndrte:priGPA']:.4f}",

f"{partial_effect_at_mean:.4f}",

],

},

)

pd.DataFrame(

{

"GPA Level": [f"At mean GPA ({mean_priGPA:.2f})"],

"Partial Effect of Attendance": [f"{partial_effect_at_mean:.4f}"],

},

)

# \nInterpretation: For a student with average prior GPA,

# Interpretation: a 1 percentage point increase in attendance rate is associated

# with a change in standardized exam score shown above.The estimated partial effect of attendance at priGPA = 2.59 is approximately 0.466. This means that for a student with an average prior GPA, a one percentage point increase in attendance rate is associated with an increase of about 0.466 points in the standardized final exam score.

Testing Significance of Partial Effect at a Specific priGPA:

We can also test whether this partial effect is statistically significant at a specific value of priGPA. We can formulate a hypothesis test for this. For example, to test if the partial effect of attendance is zero when priGPA = 2.59, we test:

We can use the f_test method in statsmodels to perform this test:

# F test for partial effect at priGPA=2.59:

# We need to create the linear combination manually

# Partial effect = beta_atndrte + 2.59 * beta_interaction

R = np.zeros((1, len(interaction_results.params)))

R[0, interaction_results.params.index.get_loc("atndrte")] = 1

R[0, interaction_results.params.index.get_loc("atndrte:priGPA")] = 2.59

ftest = interaction_results.f_test(R)

fstat = ftest.statistic

fpval = ftest.pvalue

# F-test results

pd.DataFrame(

{

"Metric": ["F-statistic", "p-value"],

"Value": [f"{fstat:.4f}", f"{fpval:.4f}"],

},

)Interpretation of Test:

The p-value for this test is approximately 0.0496, which is less than 0.05. Therefore, at the 5% significance level, we reject the null hypothesis. We conclude that the partial effect of attendance rate on standardized final exam score is statistically significantly different from zero for students with a prior GPA of 2.59.

6.2 Prediction¶

Regression models are not only used for estimating relationships between variables but also for prediction. Given values for the independent variables, we can use the estimated regression equation to predict the value of the dependent variable. This section covers point predictions, confidence intervals for the mean prediction, and prediction intervals for individual outcomes.

6.2.1 Confidence and Prediction Intervals for Predictions¶

When we make a prediction using a regression model, there are two sources of uncertainty:

Uncertainty about the population regression function: This is reflected in the standard errors of the regression coefficients and leads to uncertainty about the average value of for given values of . This is quantified by the confidence interval for the mean prediction.

Uncertainty about the individual error term: Even if we knew the true population regression function perfectly, an individual outcome will deviate from the mean prediction due to the random error term . This adds additional uncertainty when predicting an individual value of . This is quantified by the prediction interval.

The confidence interval for the mean prediction is always narrower than the prediction interval because the prediction interval accounts for both sources of uncertainty, while the confidence interval only accounts for the first source.

Let’s use the college GPA example to illustrate prediction and interval estimation.

gpa2 = wool.data("gpa2")

reg = smf.ols(formula="colgpa ~ sat + hsperc + hsize + I(hsize**2)", data=gpa2)

results = reg.fit()

# print regression table:

table = pd.DataFrame(

{

"b": round(results.params, 4),

"se": round(results.bse, 4),

"t": round(results.tvalues, 4),

"pval": round(results.pvalues, 4),

},

)

tableSuppose we want to predict the college GPA (colgpa) for a new student with the following characteristics: SAT score (sat) = 1200, high school percentile (hsperc) = 30, and high school size (hsize) = 5 (in hundreds). First, we create a Pandas DataFrame with these values:

# generate data set containing the regressor values for predictions:

cvalues1 = pd.DataFrame(

{"sat": [1200], "hsperc": [30], "hsize": [5]},

index=["newPerson1"],

)

# Prediction for Caitlin

cvalues1To get the point prediction, we use the predict() method of the regression results object:

# point estimate of prediction (cvalues1):

colgpa_pred1 = results.predict(cvalues1)

# Predicted colGPA for Caitlin

colgpa_pred1newPerson1 2.700075

dtype: float64The point prediction for college GPA for this student is approximately 2.70.

We can predict for multiple new individuals at once by providing a DataFrame with multiple rows:

# define three sets of regressor variables:

cvalues2 = pd.DataFrame(

{"sat": [1200, 900, 1400], "hsperc": [30, 20, 5], "hsize": [5, 3, 1]},

index=["newPerson1", "newPerson2", "newPerson3"],

)

# Prediction for Jeff

cvalues2# point estimate of prediction (cvalues2):

colgpa_pred2 = results.predict(cvalues2)

# Predicted colGPA for Jeff

colgpa_pred2newPerson1 2.700075

newPerson2 2.425282

newPerson3 3.457448

dtype: float64Example 6.5: Confidence Interval for Predicted College GPA¶

To obtain confidence and prediction intervals, we use the get_prediction() method followed by summary_frame().

gpa2 = wool.data("gpa2")

reg = smf.ols(formula="colgpa ~ sat + hsperc + hsize + I(hsize**2)", data=gpa2)

results = reg.fit()

# define three sets of regressor variables:

cvalues2 = pd.DataFrame(

{"sat": [1200, 900, 1400], "hsperc": [30, 20, 5], "hsize": [5, 3, 1]},

index=["newPerson1", "newPerson2", "newPerson3"],

)

# point estimates and 95% confidence and prediction intervals:

colgpa_PICI_95 = results.get_prediction(cvalues2).summary_frame(

alpha=0.05,

) # alpha=0.05 for 95% intervals

# 95% Prediction Interval

colgpa_PICI_95Interpretation of 95% Intervals:

For “newPerson1” (sat=1200, hsperc=30, hsize=5):

mean(Point Prediction): 2.700mean_ci_lowerandmean_ci_upper(95% Confidence Interval for Mean Prediction): [2.614, 2.786]. We are 95% confident that the average college GPA for students with these characteristics falls within this interval.obs_ci_lowerandobs_ci_upper(95% Prediction Interval): [1.744, 3.656]. We are 95% confident that the college GPA for a specific individual with these characteristics will fall within this much wider interval.

Let’s also calculate 99% confidence and prediction intervals (by setting alpha=0.01):

# point estimates and 99% confidence and prediction intervals:

colgpa_PICI_99 = results.get_prediction(cvalues2).summary_frame(

alpha=0.01,

) # alpha=0.01 for 99% intervals

# 99% Prediction Interval

colgpa_PICI_99As expected, the 99% confidence and prediction intervals are wider than the 95% intervals, reflecting the higher level of confidence.

6.2.2 Effect Plots for Nonlinear Specifications¶

When dealing with nonlinear models, especially those with quadratic terms or interactions, it can be helpful to visualize the predicted relationship between the dependent variable and one independent variable while holding other variables constant. Effect plots achieve this by showing the predicted values and confidence intervals for a range of values of the variable of interest, keeping other predictors at fixed values (often their means).

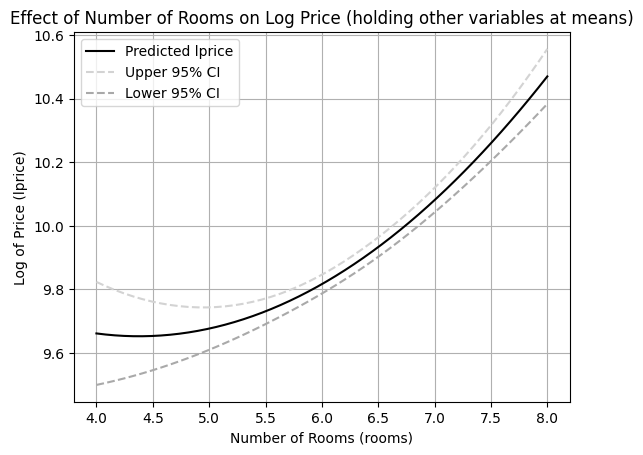

Let’s create an effect plot for the relationship between rooms and lprice from Example 6.2, holding other variables at their sample means.

hprice2 = wool.data("hprice2")

# repeating the regression from Example 6.2:

reg = smf.ols(

formula="np.log(price) ~ np.log(nox)+np.log(dist)+rooms+I(rooms**2)+stratio",

data=hprice2,

)

results = reg.fit()

# predictions with rooms = 4-8, all others at the sample mean:

nox_mean = np.mean(hprice2["nox"])

dist_mean = np.mean(hprice2["dist"])

stratio_mean = np.mean(hprice2["stratio"])

X = pd.DataFrame(

{

"rooms": np.linspace(4, 8, num=50), # Generate a range of rooms values

"nox": nox_mean,

"dist": dist_mean,

"stratio": stratio_mean,

},

)

# Design matrix for log(price) prediction

XWe create a DataFrame X where rooms varies from 4 to 8 (a reasonable range for house rooms), and nox, dist, and stratio are held at their sample means. Then, we calculate the predicted values and confidence intervals for these values of rooms.

# calculate 95% confidence interval:

lpr_PICI = results.get_prediction(X).summary_frame(alpha=0.05)

lpr_CI = lpr_PICI[

["mean", "mean_ci_lower", "mean_ci_upper"]

] # Extract mean and CI bounds

# Confidence interval for log(price)

lpr_CIFinally, we plot the predicted log price and its confidence interval against the number of rooms.

# plot:

plt.plot(

X["rooms"],

lpr_CI["mean"],

color="black",

linestyle="-",

label="Predicted lprice",

) # Plot predicted mean

plt.plot(

X["rooms"],

lpr_CI["mean_ci_upper"],

color="lightgrey",

linestyle="--",

label="Upper 95% CI", # Plot upper CI bound

)

plt.plot(

X["rooms"],

lpr_CI["mean_ci_lower"],

color="darkgrey",

linestyle="--",

label="Lower 95% CI", # Plot lower CI bound

)

plt.ylabel("Log of Price (lprice)")

plt.xlabel("Number of Rooms (rooms)")

plt.title("Effect of Number of Rooms on Log Price (holding other variables at means)")

plt.legend()

plt.grid(True) # Add grid for better readability

plt.show()

Interpretation of Effect Plot:

The plot visually represents the inverted U-shaped relationship between the number of rooms and the log of housing price, as suggested by the regression coefficients. The shaded area between the dashed lines represents the 95% confidence interval for the mean prediction. This plot helps to understand the nonlinear effect of rooms on lprice and the uncertainty associated with these predictions. Effect plots are valuable tools for interpreting and presenting results from regression models with nonlinear specifications.

6.3 Goodness-of-Fit and Model Selection¶

When working with multiple regression models, we often need to compare different specifications to determine which provides the best fit or explanatory power. This section covers tools for assessing model fit and selecting among competing models.

6.3.1 Adjusted R-Squared¶

Recall that the R-squared measures the proportion of variation in explained by the regression:

Problem with R-squared: It never decreases when adding variables, even irrelevant ones! This creates a bias toward including more variables.

Solution: Adjusted R-squared

where:

= sample size

= number of independent variables (not including intercept)

= unbiased estimate of error variance

Key Properties:

Penalizes for adding variables: can decrease when adding a variable

Compares models: Higher suggests better model (among nested models)

Can be negative: Unlike , can be negative if model fits poorly

Formula insight: always, with gap increasing as more variables are added

When to Prefer Adjusted R-squared:

Comparing models with different numbers of variables

Assessing whether an added variable improves fit enough to justify complexity

Avoiding overfitting in model selection

Example: Comparing Models with Adjusted R-squared

# Compare models with different numbers of variables

import wooldridge as woo

# Load data

hprice1 = woo.data('hprice1')

# Model 1: Simple model with key variables

model1 = smf.ols('np.log(price) ~ np.log(lotsize) + np.log(sqrft) + bdrms', data=hprice1).fit()

# Model 2: Add more variables

model2 = smf.ols('np.log(price) ~ np.log(lotsize) + np.log(sqrft) + bdrms + colonial + lprice', data=hprice1).fit()

# Model 3: Add even more variables

model3 = smf.ols('np.log(price) ~ np.log(lotsize) + np.log(sqrft) + bdrms + colonial + lprice + np.log(lotsize):bdrms', data=hprice1).fit()

# Compare fit statistics

comparison = pd.DataFrame({

'Model': ['Model 1 (3 vars)', 'Model 2 (5 vars)', 'Model 3 (6 vars)'],

'R-squared': [model1.rsquared, model2.rsquared, model3.rsquared],

'Adj R-squared': [model1.rsquared_adj, model2.rsquared_adj, model3.rsquared_adj],

'n': [model1.nobs, model2.nobs, model3.nobs],

'k': [model1.df_model, model2.df_model, model3.df_model],

'Assessment': [

'Baseline',

'Better' if model2.rsquared_adj > model1.rsquared_adj else 'Worse',

'Better' if model3.rsquared_adj > model2.rsquared_adj else 'Worse'

]

})

display(comparison.round(4))Interpretation:

R-squared increases with every variable added (mechanical property)

Adjusted R-squared may decrease if added variable doesn’t improve fit enough

Choose model with highest adjusted R-squared among reasonable specifications

6.3.2 Model Selection Criteria: AIC and BIC¶

While adjusted R-squared is intuitive, more sophisticated model selection criteria are often preferred in practice.

Akaike Information Criterion (AIC):

Bayesian Information Criterion (BIC):

Key Differences:

Penalty strength: BIC penalizes model complexity more heavily than AIC (when )

Interpretation: Lower values indicate better models (opposite of R-squared!)

Consistency: BIC is consistent (selects true model as ), AIC is not

Practical use: BIC tends to select simpler models than AIC

Example: Model Selection with AIC and BIC

# Calculate AIC and BIC for models

model_selection = pd.DataFrame({

'Model': ['Model 1', 'Model 2', 'Model 3'],

'AIC': [model1.aic, model2.aic, model3.aic],

'BIC': [model1.bic, model2.bic, model3.bic],

'Adj R-sq': [model1.rsquared_adj, model2.rsquared_adj, model3.rsquared_adj],

'Best by AIC': ['YES' if model1.aic == min([model1.aic, model2.aic, model3.aic]) else 'NO',

'YES' if model2.aic == min([model1.aic, model2.aic, model3.aic]) else 'NO',

'YES' if model3.aic == min([model1.aic, model2.aic, model3.aic]) else 'NO'],

'Best by BIC': ['YES' if model1.bic == min([model1.bic, model2.bic, model3.bic]) else 'NO',

'YES' if model2.bic == min([model1.bic, model2.bic, model3.bic]) else 'NO',

'YES' if model3.bic == min([model1.bic, model2.bic, model3.bic]) else 'NO']

})

display(model_selection.round(2))When Criteria Disagree:

AIC may prefer more complex model (lower penalty for parameters)

BIC may prefer simpler model (higher penalty for parameters)

Consider: economic theory, out-of-sample performance, interpretability

6.3.3 The Problem of Controlling for Too Many Variables¶

More variables is not always better! Over-controlling can cause problems:

1. Multicollinearity:

Adding many correlated variables inflates standard errors

Reduces statistical power to detect effects

Makes estimates unstable across samples

2. Post-treatment bias (from Chapter 3):

Including variables affected by treatment blocks causal pathways

Underestimates total effects

3. Overfitting:

Model fits sample noise instead of population relationship

Poor out-of-sample prediction

False sense of precision

4. Degrees of freedom loss:

With close to , little information for estimation

Standard errors become unreliable

R-squared artificially high

Example: Overfitting Demonstration

# Demonstrate overfitting with too many variables

np.random.seed(42)

n = 50 # Small sample

# True DGP: y depends only on x1

x1 = stats.norm.rvs(0, 1, size=n)

x_noise = stats.norm.rvs(0, 1, size=(n, 10)) # 10 irrelevant variables

y_true = 2 + 3 * x1

y = y_true + stats.norm.rvs(0, 2, size=n)

# Create dataframe

data_overfit = pd.DataFrame({'y': y, 'x1': x1})

for i in range(10):

data_overfit[f'noise{i+1}'] = x_noise[:, i]

# Simple model (correct specification)

simple_model = smf.ols('y ~ x1', data=data_overfit).fit()

# Overfit model (includes irrelevant variables)

overfit_formula = 'y ~ x1 + ' + ' + '.join([f'noise{i+1}' for i in range(10)])

overfit_model = smf.ols(overfit_formula, data=data_overfit).fit()

# Compare

overfit_comparison = pd.DataFrame({

'Model': ['Simple (True)', 'Overfit (11 vars)'],

'R-squared': [simple_model.rsquared, overfit_model.rsquared],

'Adj R-squared': [simple_model.rsquared_adj, overfit_model.rsquared_adj],

'AIC': [simple_model.aic, overfit_model.aic],

'BIC': [simple_model.bic, overfit_model.bic],

'SE(x1)': [simple_model.bse['x1'], overfit_model.bse['x1']],

'Assessment': ['Better (simpler, more precise)', 'Worse (overfit, imprecise)']

})

display(overfit_comparison.round(4))Lessons:

R-squared higher in overfit model (misleading!)

Adjusted R-squared, AIC, BIC all prefer simple model

Standard error on x1 inflated in overfit model (less precision)

Occam’s Razor: Prefer simpler models when in doubt

Guidelines for Variable Inclusion

DO include variables if:

Economic theory suggests they’re important confounders

Omitting them would cause bias in key coefficient

They significantly improve fit (F-test, adjusted R-squared)

They’re needed for policy evaluation

DON’T include variables if:

They’re post-treatment outcomes

They’re perfectly correlated with other variables

They’re only included to maximize R-squared

You’re on a “fishing expedition” for significance

Rule of Thumb: Aim for roughly to variables maximum. With , keep .

6.3.4 Log Transformation Special Cases¶

Problem with log(0):

Variables like income, sales, or participation rates can be zero. Taking is undefined!

Common “Solution”: log(1 + y)

Some researchers use to handle zeros:

# Example with zeros

income = np.array([0, 1000, 5000, 10000, 50000])

log_income_plus1 = np.log(1 + income)Problems with log(1 + y):

Interpretation changes: Coefficient no longer represents percentage change

With : 1-unit change in → percent change in

With : Interpretation unclear, especially when is large

Asymmetry: Works differently for small vs large values

Transformation more dramatic for small values

Economic implausibility: Adding 1 to income or sales lacks economic meaning

Better Alternatives:

Inverse hyperbolic sine (IHS):

Handles zeros and negatives

Approximately for large

More interpretable than

Tobit model (Chapter 17): Explicitly model zeros as censoring

Two-part model: Model (1) whether and (2) level of given

Predicting Levels from Log Models:

When dependent variable is , predicting the level of requires care:

Naive (WRONG):

Corrected (semi-log retransformation):

where .

Reason: Jensen’s inequality - when is random.

Example: Correct Prediction from Log Model

# Estimate wage equation

wage1 = woo.data('wage1')

log_wage_model = smf.ols('np.log(wage) ~ educ + exper + tenure', data=wage1).fit()

# Predict for specific person

new_person = pd.DataFrame({'educ': [16], 'exper': [10], 'tenure': [5]})

# Naive prediction (WRONG)

log_wage_pred = log_wage_model.predict(new_person)

wage_naive = np.exp(log_wage_pred.values[0])

# Corrected prediction (RIGHT)

sigma_sq = log_wage_model.mse_resid # = SSR / (n-k-1)

smearing_factor = np.exp(sigma_sq / 2)

wage_corrected = np.exp(log_wage_pred.values[0]) * smearing_factor

retransform_comparison = pd.DataFrame({

'Method': ['Predicted log(wage)', 'Naive: exp(predicted)', 'Corrected: exp(pred) * correction'],

'Value': [log_wage_pred.values[0], wage_naive, wage_corrected],

'Interpretation': [

'Log scale',

'Underestimates true expected wage',

'Proper prediction of expected wage level'

]

})

display(retransform_comparison.round(4))6.4 Residual Analysis¶

Residuals () provide crucial diagnostic information about model adequacy. Systematic patterns in residuals signal violations of Gauss-Markov assumptions.

6.4.1 What Residuals Should Look Like¶

Under the classical assumptions (MLR.1-MLR.6), residuals should:

Have mean zero (guaranteed by OLS)

Be uncorrelated with predictors (guaranteed by OLS)

Have constant variance (homoskedasticity, MLR.5)

Show no patterns when plotted against fitted values or predictors

Be approximately normal (MLR.6, less critical for large samples)

6.4.2 Residual Plots for Diagnostics¶

Plot 1: Residuals vs Fitted Values

Most important diagnostic plot! Look for:

Horizontal band: Good (homoskedasticity)

Funnel shape: Heteroskedasticity (Chapter 8)

Curved pattern: Functional form misspecification

Outliers: Influential observations

Plot 2: Residuals vs Each Predictor

Checks for:

Nonlinear relationships missed by model

Need for quadratic or interaction terms

Plot 3: Q-Q Plot (Quantile-Quantile)

Checks normality assumption:

Points on diagonal: Normal

Deviations at tails: Heavy or light tails

S-shape: Skewed distribution

Plot 4: Scale-Location Plot

Alternative check for homoskedasticity:

Plots vs fitted values

Horizontal line suggests constant variance

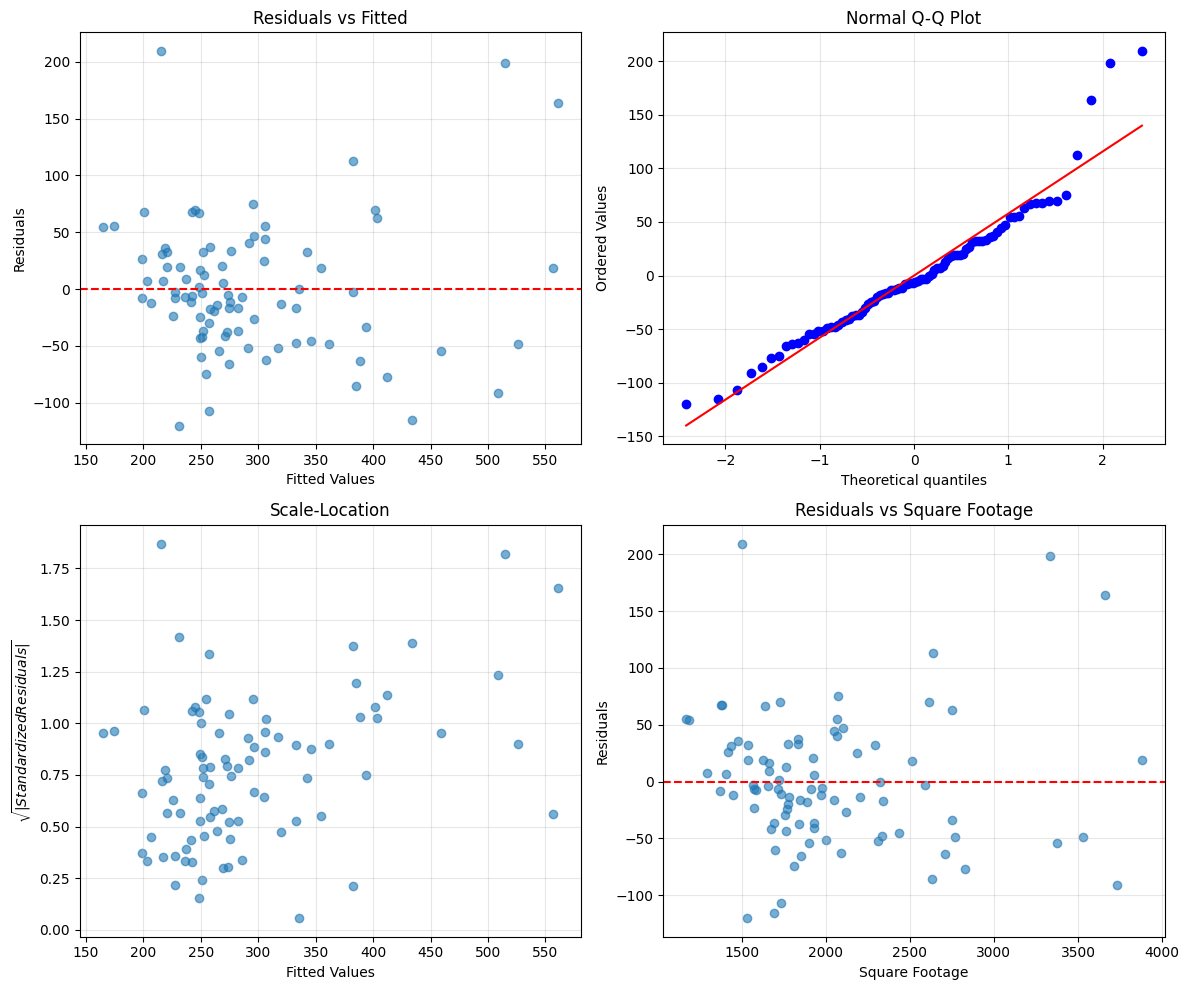

Example: Comprehensive Residual Analysis

# Estimate model

hprice1 = woo.data('hprice1')

house_model = smf.ols('price ~ lotsize + sqrft + bdrms', data=hprice1).fit()

# Get residuals and fitted values

residuals = house_model.resid

fitted = house_model.fittedvalues

standardized_resid = house_model.resid_pearson

# Create 2x2 subplot for diagnostics

fig, axes = plt.subplots(2, 2, figsize=(12, 10))

# Plot 1: Residuals vs Fitted

axes[0, 0].scatter(fitted, residuals, alpha=0.6)

axes[0, 0].axhline(y=0, color='r', linestyle='--')

axes[0, 0].set_xlabel('Fitted Values')

axes[0, 0].set_ylabel('Residuals')

axes[0, 0].set_title('Residuals vs Fitted')

axes[0, 0].grid(True, alpha=0.3)

# Plot 2: Q-Q Plot for normality

stats.probplot(residuals, dist="norm", plot=axes[0, 1])

axes[0, 1].set_title('Normal Q-Q Plot')

axes[0, 1].grid(True, alpha=0.3)

# Plot 3: Scale-Location (sqrt of standardized residuals)

axes[1, 0].scatter(fitted, np.sqrt(np.abs(standardized_resid)), alpha=0.6)

axes[1, 0].set_xlabel('Fitted Values')

axes[1, 0].set_ylabel('$\sqrt{|Standardized Residuals|}$')

axes[1, 0].set_title('Scale-Location')

axes[1, 0].grid(True, alpha=0.3)

# Plot 4: Residuals vs sqrft (key predictor)

axes[1, 1].scatter(hprice1['sqrft'], residuals, alpha=0.6)

axes[1, 1].axhline(y=0, color='r', linestyle='--')

axes[1, 1].set_xlabel('Square Footage')

axes[1, 1].set_ylabel('Residuals')

axes[1, 1].set_title('Residuals vs Square Footage')

axes[1, 1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

How to Interpret:

Funnel in residuals vs fitted → Heteroskedasticity (use robust SEs, Chapter 8)

Curved pattern → Add quadratic/interaction terms

Deviations from Q-Q diagonal → Non-normal errors (okay if is large)

Few extreme outliers → Check for data errors or influential observations

6.4.3 Identifying Influential Observations¶

Some observations have disproportionate influence on regression results. Key diagnostics:

1. Leverage: How far is from

High leverage observation can pull regression line

2. Studentized Residuals: Residuals standardized by their standard error

suggests outlier

3. Cook’s Distance: Combined measure of leverage and residual size

suggests influential observation

is very influential

Example: Influence Diagnostics

# Calculate influence measures

from statsmodels.stats.outliers_influence import OLSInfluence

influence = OLSInfluence(house_model)

leverage = influence.hat_matrix_diag

cooks_d = influence.cooks_distance[0]

studentized_resid = influence.resid_studentized_internal

# Identify influential observations

influential = pd.DataFrame({

'Observation': range(len(leverage)),

'Leverage': leverage,

'Cooks D': cooks_d,

'Stud. Resid': studentized_resid,

'Influential': (cooks_d > 4/len(leverage)) | (np.abs(studentized_resid) > 3)

})

# Show top 5 most influential

top_influential = influential.nlargest(5, 'Cooks D')

display(top_influential.round(4))

# Plot Cook's Distance

plt.figure(figsize=(10, 4))

plt.stem(range(len(cooks_d)), cooks_d, markerfmt=',', basefmt=' ')

plt.axhline(y=4/len(leverage), color='r', linestyle='--', label='Threshold (4/n)')

plt.xlabel('Observation Index')

plt.ylabel("Cook's Distance")

plt.title("Influence Plot: Cook's Distance")

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()What to Do with Influential Observations:

Check for data errors: Typos, incorrect units, etc.

Investigate substantively: Are they legitimate unusual cases?

Report sensitivity: Show results with and without influential observations

Use robust methods: Robust regression (less sensitive to outliers)

DON’T automatically delete: May represent important heterogeneity

Residual Analysis Best Practices

Always:

Plot residuals vs fitted values (most important!)

Check for a few influential observations

Investigate any clear patterns

Often:

Plot residuals vs key predictors

Check Q-Q plot if assuming normality

Calculate Cook’s distance for leverage

Sometimes:

Use formal tests (Breusch-Pagan, White for heteroskedasticity)

Apply transformations based on residual patterns

Refit model excluding highly influential observations

Never:

Delete observations just to improve R-squared

Ignore systematic patterns in residuals

Assume residuals are fine without checking

Chapter Summary¶

This chapter covered essential practical issues in multiple regression analysis, focusing on model specification, functional form, and diagnostic checking. These tools help you build better models and avoid common pitfalls.

Key Concepts:

1. Effects of Data Scaling (Section 6.1.1-6.1.2):

Multiplying by constant scales , , and by same constant

Multiplying by constant scales and by reciprocal

t-statistics and R-squared are invariant to scaling

Standardized coefficients (beta coefficients) allow comparing importance across variables

2. Functional Form (Section 6.1.3-6.1.6):

Log transformations: Interpret coefficients as percentage effects, invariant to scaling

Log-linear: = percentage change in per unit change in

Log-log: = elasticity (percentage change in per 1% change in )

Quadratic terms: Allow nonlinear (U-shaped or inverted-U) relationships

Interaction terms: Allow effect of to depend on level of

3. Goodness-of-Fit and Model Selection (Section 6.3):

Adjusted R-squared penalizes adding variables, prefer for model comparison

AIC and BIC: Lower is better, BIC penalizes complexity more heavily

Too many variables: Causes multicollinearity, overfitting, imprecise estimates

Occam’s Razor: Prefer simpler models when fit is similar

4. Special Issues with Logs (Section 6.3.4):

log(1 + y) has interpretation problems - avoid when possible

Inverse hyperbolic sine better for handling zeros

Predicting levels from log(y): Need retransformation correction

5. Prediction (Section 6.2):

Confidence interval for : Narrower, estimates mean

Prediction interval for new : Wider, accounts for individual variation

Prediction intervals always wider than confidence intervals by factor of

6. Residual Analysis (Section 6.4):

Residual plots reveal violations of assumptions

Patterns suggest heteroskedasticity or functional form problems

Cook’s distance identifies influential observations

Always check residuals before trusting results!

Practical Workflow for Model Building:

Start simple: Begin with linear specification, key variables

Check residuals: Look for patterns suggesting needed transformations

Add complexity thoughtfully: Quadratics, interactions, logs as theory/diagnostics suggest

Compare models: Use adjusted R-squared, AIC, BIC

Test restrictions: F-tests for joint significance of added terms

Validate: Check out-of-sample performance, sensitivity to outliers

Interpret carefully: Remember scaling, functional form implications

Common Mistakes to Avoid:

✗ Including too many variables (overfitting)

✗ Chasing high R-squared without theory

✗ Ignoring residual patterns

✗ Misinterpreting log coefficients

✗ Using prediction intervals when you need confidence intervals (or vice versa)

✗ Deleting influential observations without investigation

Connections to Other Chapters:

Chapter 3: Bad controls, multicollinearity, functional form as specification issues

Chapter 5: Model selection relates to consistency (correct specification)

Chapter 8: Heteroskedasticity revealed by residual analysis, affects prediction intervals

Chapter 9: RESET test for functional form, proxy variables

Looking Forward:

Chapter 7: Dummy variables (discrete functional form)

Chapter 8: Heteroskedasticity (variance patterns in residuals)

Chapter 9: Specification tests (formal checks of functional form)

The Bottom Line:

Regression is an art as much as a science. Good practice combines:

Economic theory: What variables and functional forms make sense?

Diagnostic checking: Do residuals reveal problems?

Model comparison: Which specification fits best without overfitting?

Robust inference: Use methods that work even when assumptions fail

Master these tools and you’ll build better, more reliable regression models!